This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The oil and gas boom in the United States was made possible by the extensive credit afforded to drillers. As is the nature of the junk-bond market, lots of money flowed to companies with much riskier drilling prospects than, say, the oil majors. The situation will compound itself if oilprices stay low.

Oilprices fell back suddenly over the last few trading sessions, dragged down by some forces beyond the oil market. dollar has helped drive up crude prices for weeks , but that came to an abrupt halt last week. A rebound for the greenback led to a steep decline in oilprices on Friday.

As oilprices remain unsteady and OPEC continues to make headlines every hour, the world is focused on oil’s immediate future. In a speech made at the Association of International Petroleum Negotiators’ 2017 International Petroleum Summit, Johnston laid out his concerns for the future of oil.

The Review captures the significant impact the global pandemic had on energy markets and how it may shape future global energy trends. This fall was driven mainly by oil, which accounted for almost three quarters of the net decline. World oil production fell for the first time since 2009 by 6.6 million b/d) and non-OPEC (-2.3

The demand for oil in 2015 will drop to its lowest level since 2002 because of an oversupply of crude and stagnant economies in China and Europe, according to OPEC’s latest forecast. OPEC’s monthly report said demand for the cartel’s oil will fall to 28.9 Futures for US crude also are down dramatically. Market Background Oil'

In the Douglas-Westwood Monday note , Andy Jenkins from the energy research group’s London office observes that the decline in oilprices may impact deepwater production and in particular a key future enabler: subsea processing (SSP).

Two diametrically opposed views dominate the current debate about where the oilprice is heading. On the other hand, however, there is the view that the price of oil is set to explode, primarily due to underinvestment in the upkeep of brownfields , development of greenfields , and exploration for new resources.

Saudi Arabia has long enjoyed the status of being the top crude oil exporter in the world. With record production of 10.564 million barrels per day in June 2015, Saudi Arabia has been one of the major driving forces behind the current oilprice slump. This could eventually result in refiners cutting their crude oil imports.

It may be difficult to look beyond the current pricing environment for oil, but the depletion of low-cost reserves and the increasing inability to find major new discoveries ensures a future of expensive oil. The industry did not log a single “giant” oil field.

The impact of rising oilprices on North American light tight oil (LTO) production is said to be a “Catch 22”, the title of Joseph Heller’s popular 1961 novel set in WWII. Too many analysts continue to believe drilling and service has the same problem with rising oilprices. by David Yager for Oilprice.com.

Predicting and diagnosing the trajectory of oilprices has become something of a cottage industry in the past year. But along with all of the excess crude flowing from the oil patch, there is also an abundance of market indicators that while important, tend to produce a lot of noise that makes any accurate estimate nearly impossible.

dollar has jumped to its strongest level in nearly a year, raising questions about how a strong greenback could act as a drag on debt and oil demand in much of the world. dollar to go up, which is putting downward pressure on prices,” Phil Flynn, analyst at PriceFutures Group in Chicago, told Reuters. But the U.S.

Oilprices faltered at the start of the second week of the year, as fears set in about a rapid rebound in US shale production. percent in intraday trading on Monday, after a report at the end of last week showed another solid build in the US rig count, the tenth consecutive week that the oil industry added rigs back into the field.

IEO2014 projections of future liquids balances include two broad categories: crude and lease condensate and other liquid fuels. Crude and lease condensate includes tight oil, shale oil, extra-heavy crude oil, field condensate, and bitumen (i.e., oil sands, either diluted or upgraded). oil shale), and refinery gain.

OPEC says that $10 trillion worth of investment will need to flow into oil and gas through 2040 in order to meet the world’s energy needs. The OPEC published its World Oil Outlook 2015 (WOO) in late December, which struck a much more pessimistic note on the state of oil markets than in the past. mb/d between 2020 and 2025, 3.3

World oil production capacity to 2020 (crude oil and NGLs, excluding biofuels). Oil production capacity is surging in the United States and several other countries at such a fast pace that global oil output capacity could grow by nearly 20% from the current 93 million barrels per day to 110.6 Source: Maugeri 2012.

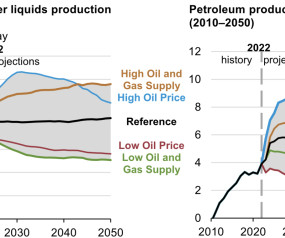

EIA projects that the United States will continue to be an integral part of global oil markets and a significant source of supply in these cases, as increased exports of finished products support US production. It reflects laws and regulations adopted through mid-November 2022 but assumes no new laws or regulations in the future.

Short-term oil demand is still growing strong and will continue to do so through the end of 2020 despite the market’s increasing focus on electric vehicles and the forecasted future plateau in oil demand, according to new analysis from IHS Markit, a global business information provider. Source: IHS Markit 2018.

Proponents of the concept of peak oil supply argue that the world faces a situation—possibly very soon—in which its capacity to produce oil hits a ceiling, with demand subsequently having to adjust as supply begins to decline and alternatives to oil move into the market to fill the gap. Earlier post.).

Global oil and gas companies are increasingly facing an uphill battle as global warming policies are taking their toll. Most analysts and market watchers are focusing on peak oil demand scenarios, but the reality could be much darker. by Cyril Widdershoven for Oilprice.com.

Change in primary oil demand by sector and region in the central New Policies Scenario, 2010-2035. Under the WEO 2011 central scenario, oil demand rises from 87 million barrels per day (mb/d) in 2010 to 99 mb/d in 2035, with all the net growth coming from the transport sector in emerging economies. Click to enlarge. billion in 2035.

World oilprices remain high in the IEO2011 Reference case, but oil consumption continues to grow; both conventional and unconventional liquid supplies are used to meet rising demand. In the IEO2011 Reference case the price of light sweet crude oil (in real 2009 dollars) remains high, reaching $125 per barrel in 2035.

However, the new forecast represents a slowing of futureoil sands production growth compared to the predictions of last year’s forecast. According to CAPP’s 2014 Crude Oil Forecast, Markets and Transportation , total Canadian crude oil production will increase to 6.4 CAPP forecast. Click to enlarge. In 2013, 1.9

A new study by the Peterson Institute for International Economics concluded that the Kerry-Lieberman “American Power Act”—the energy and climate change legislation recently introduced in the Senate ( earlier post )—would reduced US oil imports by 33-40% below current levels and by 9-19% below projected business-as-usual levels by 2030.

Conventional oil and gas discoveries during the past three years are at the lowest levels in seven decades and a significant rebound is not expected, according to a new report by global business information provider IHS Markit. —Keith King, senior advisor at IHS Markit and a lead author of the IHS Markit E&P trends analysis.

When reports emerged that India and China are in talks about forming an oil buyers’ club , OPEC was probably too busy with its upcoming June 22 meeting to concern itself with that dangerous alliance. What’s more, they might not be alone in this attempt to curb OPEC’s clout on the global oil market. The timing is right. The boom in U.S.

Many oil companies had trimmed their budgets heading into 2015 to deal with lower oilprices. But the collapse of prices in July—owing to the Iran nuclear deal, an ongoing production surplus, and economic and financial concerns in Greece and China—have darkened the mood. by Nick Cunningham of Oilprice.com.

Chevron’s focus on optimizing the thermal management of the Kern River field has resulted in a steady drop in the steam:oil ratio (barrels steam water per barrel oil), resulting in improved economics of the field even with slowly declining production. Data: California DOGGR. Click to enlarge. Source: Chevron. Click to enlarge.

In a newly released report, market analyst Visiongain has calculated the Arctic oil and gas exploration and production market to be worth $11.93 Although oil and gas have been produced in the Arctic region for years, many of the vast oil and gas fields that initiated interest in the Arctic are in decline.

shale has thrown in another unknown in the mix of factors driving the price of oil. This year, shale output forecasts combine with OPEC’s production cuts, geopolitical factors, and unexpected outages to further complicate supply/demand and oilprice forecasts by Wall Street’s major investment banks. In recent years, U.S.

Global demand for oil may well peak before 2020, falling back to levels significantly below 2010 demand by 2035, according to a multi-client research study conducted by Ricardo Strategic Consulting launched in June 2011 in association with Kevin J. The world is nearing a paradigm shift in oil demand. Lindemer LLC.

While OPEC mulls over further steps to once again support falling oilprices, tech startups are quietly ushering in a new era in oil and gas: the era of the digital oil field. The Internet of Things is entering oil and gas, and so are analytics and artificial intelligence. by Irina Slav for Oilprice.com.

Examples of emerging oil sands related technologies and trade-offs. The paper is an examination of how various choices about the scale of the life cycle analysis applied to oil sands (i.e., The source material is neither oil nor tar but bitumen, but is most generally described as an example of ultraheavy oil.”.

The Oil War Is Only Just Getting Started. It’s been a month now that investors and analysts have been closely watching two main drivers for oilprices: how OPEC is doing with the supply-cut deal, and how US shale is responding to fifty-plus-dollar oil with rebounding drilling activity.

In contrast to arguments that peak conventional oil production is imminent due to physical resource scarcity, a team from Stanford University and UC Santa Cruz has examined the alternative possibility of reduced oil use due to improved efficiency and oil substitution. 2010, to above 140 $/bbl in constant 2010 dollars).

The IEA June 2022 Oil Market Report (OMR) forecasts world oil demand to reach 101.6 While higher prices and a weaker economic outlook are moderating consumption increases, a resurgent China will drive gains next year, with growth accelerating from 1.8 Since 6 June, WTI and Brent futures have averaged above $120/bbl.

This long-term growth is expected to be propelled by improving vehicle technology economics—a function of battery innovations, government transportation energy policies, oilprice projections, and movements to price carbon. —Scott Shepard, senior research analyst with Navigant Research.

The second quarter of 2020 will see the largest volume of liquids production cuts, including shut-in production, in the history of the oil industry, according to IHS Markit. The Great Shut-In, a rapid and brutal adjustment of global oil supply to a lower level of demand is underway. Some will be impacted more than others.

When reports emerged that India and China are in talks about forming an oil buyers’ club , OPEC was probably too busy with its upcoming June 22 meeting to concern itself with that dangerous alliance. What’s more, they might not be alone in this attempt to curb OPEC’s clout on the global oil market. The timing is right. The boom in U.S.

Energy executives expect continued volatility in the price-per-barrel of oil for the remainder of the year, with 64% predicting crude prices to exceed $121 per barrel. Only 35% think current crude prices are near the high they expect for oil this year, predicting the peak will be between $111 and $120 per barrel.

Due to the collapse in oilprices, IHS Markit expects US producers are in the process of curtailing about 1.75 The oil market fear that characterized March and the extreme price pressure that producers felt in April have galvanized producers across North America into unprecedented action. However, nearly 1.4

Canadian Oil Sands Trust, the largest stakeholder (36.74%) in the Syncrude oil sands project, announced plans to increase the synthetic crude oil production capacity at Syncrude Mildred Lake upgrader to 425,000 barrels per day by 2020 from 350,000 now. Marcel Coutu, Canadian Oil Sands’ President and CEO. and Imperial Oil.

In the paper, Nataliya Malyshkina and Deb Niemeier point out that the peak of oil production is estimated to occur approximately between 2010 and 2030, and note that all those dates are considerably earlier than their estimate of the time until renewable replacement technologies are viable in the market (around 2140).

The Brent crude oil spot price averaged $112 per barrel in 2012, and EIA’s July 2013 Short-Term Energy Outlook projects averages of $105 per barrel in 2013 and $100 per barrel in 2014. The largest components of future non-petroleum liquid fuels production are biofuels in Brazil and the United States, at 0.7 Liquid fuels.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content