This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Junk-bond debt in energy has reached $210 billion, which is about 16 percent of the $1.3 That is a dramatic rise from just 4 percent that energy debt represented 10 years ago. As is the nature of the junk-bond market, lots of money flowed to companies with much riskier drilling prospects than, say, the oil majors.

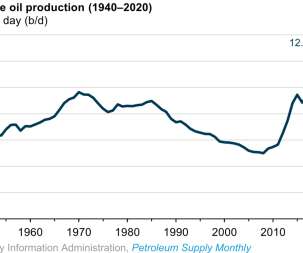

US crude oil production averaged 11.3 million b/d in 2019, according to the US Energy Information Administration (EIA). The production decline resulted from reduced drilling activity related to low oilprices in 2020. In January 2020, US crude oil production reached a peak of 12.8 million b/d. million b/d in 2020.

Oilprices have climbed by about 50 percent from their February lows, topping $40 per barrel. But the rally could be reaching its limits, at least temporarily, as persistent oversupply and the prospect of new shale production caps any potential price increase. by Nick Cunningham of Oilprice.com. More output is bearish.”

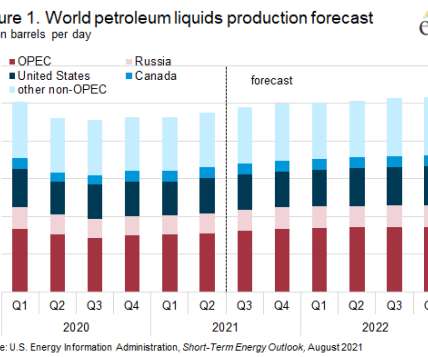

The US Energy Information Administration (EIA) August Short-Term Energy Outlook (STEO) forecasts that US crude oil production will average 10.7 Source: US Energy Information Administration, Short-Term Energy Outlook, August 2018. Source: US Energy Information Administration, Short-Term Energy Outlook, August 2018.

Oil production capacity is surging in the United States and several other countries at such a fast pace that global oil output capacity could grow by nearly 20% from the current 93 million barrels per day to 110.6 Such an increase in capacity could prompt a plunge or even a collapse in oilprices, he suggests.

Industry appetite for oil-rich resource plays, particularly the NorthDakota Bakken shale, Texas Eagle Ford shale and Ohio Utica shale, drove deal activity in the unconventional sector to a record $62 billion. We expect continued strong activity in oil and liquids-rich resource plays in 2012. —Ronyld W.

Argentina offers one of the few places on earth where oil companies are not suffering from the full force of the collapse in prices. Argentina regulates oilprices, a policy originally intended to insulate the public from the whims of the market, protecting people from triple-digit crude prices.

The financial pages of Canadian newspapers have been full of headlines lately announcing the potential of two large shale oil fields in the Northwest Territories said to contain enough oil to rival the Bakken Formation of NorthDakota and Montana. enthused the Financial Post. “NEB WTI crude closed at $59.13

Oilprices have rebounded strongly since March. The benchmark WTI prices soared by more than 36 percent in two months, and Brent has jumped by more than 25 percent. Diamondback Energy, another Permian operator, may add two rigs this year. Lower prices would then force further cut backs in rigs and spending.

Over the long term, lower-than-expected oilprices could affect the outlook for oil sands production, and in certain scenarios higher transportation costs resulting from pipeline constraints could exacerbate the impacts of low prices. Rail Direct to the Gulf Coast Scenario.

. … President Biden has made clear that he wants Americans to have access to affordable and reliable energy, including at the pump. … We are engaging with relevant OPEC+ members on the importance of competitive markets in setting prices. As a result, EIA’s crude oilprice forecast remains mostly unchanged from the July STEO.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content