This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The collapse in world oilprices in the second half of 2014 will have only a moderate impact on the fast-developing low-carbon transition in the world electricity system, according to research firm Bloomberg New Energy Finance. However, the slump in the Brent crude price per barrel from $112.36 on 30 June to $61.60

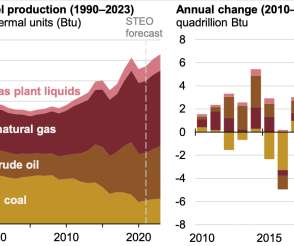

After declining in 2020, the combined production of US fossil fuels (including natural gas, crude oil, and coal) increased by 2% in 2021 to 77.14 Crude oil accounted for 30%, coal for 15%, and natural gas plant liquids (NGPLs) for 9%. In 2020, US coal production had fallen to its lowest level since 1964.

The US Energy Information Administration (EIA) forecasts that US crude oil production will average 11.9 Despite the increases in production, EIA expects the Brent crude oilprice to remain above $100 per barrel this year, according to the agency’s May 2022 Short-Term Energy Outlook (STEO). million barrels per day set in 2019.

Oil remains the world’s leading fuel, but its 33.1% Coal’s market share of 30.3% Oil demand grew by less than 1%—the slowest rate amongst fossil fuels—while gas grew by 2.2%, and coal was the only fossil fuel with above average annual consumption growth at 5.4% World primary energy consumption grew by 2.5%

EIA expects crude oilprices to decrease through 2023 and 2024, even as petroleum consumption increases, largely because growth in crude oil production in the United States and abroad will continue to increase over the next two years. Areas of uncertainty include Russian oil supply and OPEC production. per gallon in 2024.

Ceres recently released a new report concluding that coal-to-liquid (CTL) and oil shale technologies face significant environmental and financial obstacles—from water constraints, to technological uncertainties to regulatory and market risks—that pose substantial financial risks for investors involved in such projects.

Crude and lease condensate includes tight oil, shale oil, extra-heavy crude oil, field condensate, and bitumen (i.e., oil sands, either diluted or upgraded). Other liquids refer to natural gas plant liquids (NGPL), biofuels (including biomass-to-liquids [BTL]), gas-to-liquids (GTL), coal-to-liquids (CTL), kerogen (i.e.,

DICE involves converting coal or biomass into a water-based slurry (called micronised refined carbon, MRC) that is directly injected into a large, specially adapted diesel engine. CSIRO is excited about the potential for DICE to lower power costs, halve carbon dioxide intensity and create a new export market for both brown and black coal.

World oilprices remain high in the IEO2011 Reference case, but oil consumption continues to grow; both conventional and unconventional liquid supplies are used to meet rising demand. In the IEO2011 Reference case the price of light sweet crude oil (in real 2009 dollars) remains high, reaching $125 per barrel in 2035.

Profound shifts in the regional distribution of oil demand and supply growth will redefine the refining industry and transform global oil trade over the next five years, according to the annual Medium-Term Oil Market Report (MTOMR) released by the International Energy Agency (IEA). The oil market is at a crossroads.

The National Energy Technology Laboratory (NETL) has released a follow-on study to its 2009 evaluation of the economic and environmental performance of Coal-to-Liquids (CTL) and CTL with modest amounts of biomass mixed in (15% by weight) for the production of zero-sulfure diesel fuel. This equates to diesel prices in the range of $2.70

Australia’s Syngas Limited has engaged Rentech to provide Fischer-Tropsch fuels production preliminary engineering services for Syngas’ proposed commercial scale coal and biomass to liquids (CBTL) fuels facility in Southern Australia, known as the Clinton Project. Additionally, the Clinton coal fluidizes well. Gas Conditioning.

China is about to become the largest oil-importing country and India becomes the largest importer of coal by the early 2020s. The Middle East becomes the world’s second-largest gas consumer by 2020 and third-largest oil consumer by 2030, redefining its role in global energy markets. Mobility and oil. Source: IEA.

SES and Zuari have been investigating business development opportunities where SES’ U-GAS technology for coal gasification can be integrated into industrial projects in India, including the potential for application of the U-GAS technology in Zuari’s own industrial plants and potential plant expansions.

Comparison of coal consumption and CO 2 emissions for co-production and separate production of liquids and power. Conventional CTL plant gasifies coal to produce a syngas which is then converted in a Fischer-Tropsch reactor to products. Even with CCS, the liquid product costs are comparable to recent crude oilprices.

Domestic crude oil production increases sharply in the AEO2014 Reference case, with annual growth averaging 0.8 While domestic crude oil production is projected to level off and then slowly decline after 2020 in the Reference case, natural gas production grows steadily, with a 56% increase between 2012 and 2040, when production reaches 37.6

The Brent crude oil spot price averaged $112 per barrel in 2012, and EIA’s July 2013 Short-Term Energy Outlook projects averages of $105 per barrel in 2013 and $100 per barrel in 2014. Biomass Climate Change Coal-to-Liquids (CTL) Emissions Forecasts Fuels Gas-to-Liquids (GTL) Market Background' Liquid fuels.

Change in primary oil demand by sector and region in the central New Policies Scenario, 2010-2035. Under the WEO 2011 central scenario, oil demand rises from 87 million barrels per day (mb/d) in 2010 to 99 mb/d in 2035, with all the net growth coming from the transport sector in emerging economies. Click to enlarge. billion in 2035.

Examples of emerging oil sands related technologies and trade-offs. The paper is an examination of how various choices about the scale of the life cycle analysis applied to oil sands (i.e., The source material is neither oil nor tar but bitumen, but is most generally described as an example of ultraheavy oil.”.

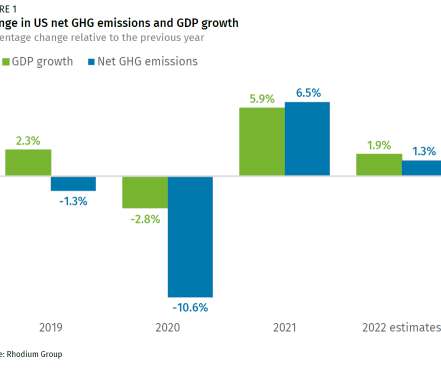

Despite efforts to continue stimulating the US economy in the wake of the pandemic, high inflation put a damper on economic growth, which was exacerbated by a spike in oilprices as a result of Russia’s invasion of Ukraine. Consequently, the US economy grew 1.9% in 2022, down from a 5.7% GDP increase in 2021.

The break-even crude oilprice for a delivered biomass cost of $94/metric ton when hydrogen is derived from coal, natural gas or nuclear energy ranges from $103 to $116/bbl for no carbon tax and even lower ($99–$111/bbl) for the carbon tax scenarios. —Singh et al.

Under the Reference case, domestic crude oil production is expected to grow by more than 20% over the coming decade; already, domestic crude oil production increased from 5.1 Over the next 10 years, continued development of tight oil (e.g., Over the next 10 years, continued development of tight oil (e.g.,

Renewables will be the primary source for new electricity generation, but natural gas, coal, and increasingly batteries will be used to help meet load and support grid reliability. Oil and natural gas production will continue to grow, mainly to support increasing energy consumption in developing Asian economies. —Stephen Nalley.

In contrast to arguments that peak conventional oil production is imminent due to physical resource scarcity, a team from Stanford University and UC Santa Cruz has examined the alternative possibility of reduced oil use due to improved efficiency and oil substitution. 2010, to above 140 $/bbl in constant 2010 dollars).

The five different fuel groups were those derived: from conventional petroleum; from unconventional petroleum; synthetically from natural gas, coal, or combinations of coal and biomass via the FT process; renewable oils; and alcohols. million bpd. Reduced GHG impact. For CTL, life-cycle GHG emissions would roughly double.

Energy executives expect continued volatility in the price-per-barrel of oil for the remainder of the year, with 64% predicting crude prices to exceed $121 per barrel. Only 35% think current crude prices are near the high they expect for oil this year, predicting the peak will be between $111 and $120 per barrel.

Natural gas is projected to be the fastest growing fossil fuel, and coal and oil are likely to lose market share as all fossil fuels experience lower growth rates. OECD oil demand peaked in 2005 and in 2030 is projected to be roughly back at its level in 1990. Oil, excluding bio-fuels, will grow relatively slowly at 0.6%

Coal accounted for 45% of total energy-related CO 2 emissions in 2011, followed by oil (35%) and natural gas (20%). China made the largest contribution to the global increase, with its emissions rising by 720 million tonnes (Mt), or 9.3%, primarily due to higher coal consumption. This represents an increase of 1.0 In 2011, a 6.1%

In addition to high oilprices and the financial crisis, the increased use of new renewable energy sources, such as biofuels for road transport and wind energy for electricity generation, had a noticeable and mitigating impact on CO 2 emissions. Fossil oil consumption decreased by one per cent, due to high prices and more biofuels.

savings stimulated by high oilprices led to a decrease of 3% in CO 2 emissions in the European Union and of 2% in both the United States and Japan. tonnes per capita, despite a decline due to the recession in 2008-2009, high oilprices and an increased share of natural gas. Coal consumption in China increased by 9.7%

In their analysis, the authors examined the effect of 5 factors on EDV deployment: crude oil and natural gas prices; a federal CO 2 policy; a federal renewable portfolio standard (RPS); and EDV battery cost. No EDV deployment occurs with high battery costs, low oilprices, and no CO 2 policy.

If the US military increases its use of alternative jet and naval fuels that can be produced from coal or various renewable resources, including seed oils, waste oils and algae, there will be no direct benefit to the nation’s armed forces, according to a new RAND Corporation study.

However, the US military can play an important role in promoting stability in major oil producing regions and by helping protect the flow of energy through major transit corridors and on the high seas, the reports suggest. In the lead report, Bartis notes that global oil supplies are finite and thus, at some point, oil production must peak.

Dimethyl ether is a diesel fuel replacement that can be produced from abundant resources including natural gas, landfill methane, coal and biomass. At current oilprices, DME can be produced and distributed at less than 1/2 the cost of conventional fuel.

The fortunes of alternative energy have historically waxed and waned with the price levels of oil, gas, and other energy sources, rising when prices are high only to fall once they retreat. Base case economics for EVs in North America are very challenging, absent significant disruption in oilprice or battery cost.

The WEO finds that the extraordinary growth in oil and natural gas output in the United States will mean a sea-change in global energy flows. barely rises in OECD countries, although there is a pronounced shift away from oil, coal (and, in some countries, nuclear) towards natural gas and renewables. Oil demand reaches 99.7

World production of fossil fuels—oil, coal, and natural gas—increased 2.9% million tons of oil equivalent (Mtoe) per day, according to a Worldwatch Institute analysis. Energy prices reflected this shift: oil peaked at $144 per barrel in July, then fell to $34 per barrel in December. Oil production reached 10.7

Electrification will also reduce oil dependence, providing foreign policy benefits and the potential to reduce real oilprices and oilprice volatility. With the current fuel mix of the US power sector (about half coal, about 30% “carbon-free”), CO 2 emissions for HEVs and EVs are similar. Policy options.

However, the study found that the growth of CO 2 emissions by 2030 would only be 1-5% lower than if subsidies had been maintained, regardless of whether oilprices are low or high. First, these subsidies generally apply only to oil, gas, and electricity. This is facilitated by today’s low oilprices.

AEO2013 offers a number of other key findings, including: Crude oil production , especially from tight oil plays, rises sharply over the next decade. Domestic oil production will rise to 7.5 Biofuels grow at a slower rate due to lower crude oilprices and. Overall findings. Biomass and biofuels growth is slower.

The Annual Energy Outlook 2011 (AEO2011) Reference case released yesterday by the US Energy Information Administration (EIA) more than doubles the technically recoverable US shale gas resources assumed in AEO2010 and added new shale oil resources. US crude oil production increases from 5.4 trillion cubic feet in 2009 to 9.4

Background colors of the cells represent the crude oilprice required for economic feasibility. These synthetic fuels are economically competitive with petro-diesel when the crude oilprice (COP) is at or above $86 per barrel (based on a 20% rate of return, in January 2008 dollars, with a carbon price of zero).

The Annual Energy Outlook 2015 (AEO2015) released today by the US Energy Information Administration (EIA) projects that US energy imports and exports will come into balance—a first since the 1950s—because of continued oil and natural gas production growth and slow growth in energy demand. Tcf in the High Oil and Gas Resource case.

California’s LCFS also would have little or no impact on GHG emissions nationwide and would harm our nation’s energy security by discouraging the use of Canadian crude oil—our nation’s largest source of crude—and ethanol produced in the American Midwest. By regulating the fuel pathway of transportation fuels—i.e., NPRA President Charles T.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content