This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The collapse in world oilprices in the second half of 2014 will have only a moderate impact on the fast-developing low-carbon transition in the world electricity system, according to research firm Bloomberg New Energy Finance. However, the slump in the Brent crude price per barrel from $112.36 on 30 June to $61.60

Oilprices fell back suddenly over the last few trading sessions, dragged down by some forces beyond the oil market. dollar has helped drive up crude prices for weeks , but that came to an abrupt halt last week. A rebound for the greenback led to a steep decline in oilprices on Friday.

Oxford Catalysts Group PLC has been selected to supply Calumet Specialty Product Partners, L.P. Calumet intends to provide the majority, if not all of the funding for this project, and to start production in the second half of 2014. Any remaining funding will be provided by Calumet’s other project partners.

Two diametrically opposed views dominate the current debate about where the oilprice is heading. Why the price of oil could spike before that. That leaves the period until the end of the 2020s, during which we believe overall oil demand will continue to grow (albeit slower than before). Since (non-U.S.

It may be difficult to look beyond the current pricing environment for oil, but the depletion of low-cost reserves and the increasing inability to find major new discoveries ensures a future of expensive oil. However, now that oilprices are so low, oil companies have no room to boost spending.

Oilprices appear to be stuck in the $50s per barrel, but that doesn’t mean there aren’t serious supply risks to the market. An unexpected disruption could occur at any moment, as has happened in the past, leading to a sudden and sharp jump in prices. The most near-term supply risk comes from Iraq. bank Citi said.

Despite what appears to be a saturated oil market in 2014, oil producers around the world will struggle to meet rising demand over the next few decades. Under that assumption, oilprices would rise only a modest amount over that timeframe. by Nick Cunningham of Oilprice.com. million bpd by 2035.

The impact of rising oilprices on North American light tight oil (LTO) production is said to be a “Catch 22”, the title of Joseph Heller’s popular 1961 novel set in WWII. Too many analysts continue to believe drilling and service has the same problem with rising oilprices. by David Yager for Oilprice.com.

Lest we be too quick to forget whence we came, America is now 9-months into lower gasoline prices, which started their swoon the week of June 30, 2015 from a lofty national average just under $3.70, tumbling almost every subsequent week before bottoming and bouncing from $2.02 quota, with oil already allocated away from the U.S.,

The OPEC published its World Oil Outlook 2015 (WOO) in late December, which struck a much more pessimistic note on the state of oil markets than in the past. On the one hand, OPEC does not see oilprices returning to triple-digit territory within the next 25 years, a strikingly bearish conclusion.

Those claiming that oil will continue to fall from here and remain low for evermore, however, are flying in the face of both history and common sense. The question we should be asking ourselves is not if oilprices will recover, but when they will. There is no doubt that supply has increased.

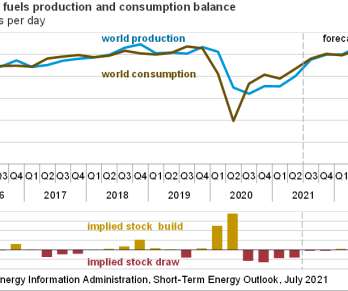

Total global oil production could decline for the next several years in a row as scarce new sources of supply come online. According to data from Rystad Energy, overall global oil output will fall this year as natural depletion overwhelms all new sources of supply. The price acts as a self-correcting mechanism.

Many oil companies had trimmed their budgets heading into 2015 to deal with lower oilprices. But the collapse of prices in July—owing to the Iran nuclear deal, an ongoing production surplus, and economic and financial concerns in Greece and China—have darkened the mood. by Nick Cunningham of Oilprice.com.

Profound shifts in the regional distribution of oil demand and supply growth will redefine the refining industry and transform global oil trade over the next five years, according to the annual Medium-Term Oil Market Report (MTOMR) released by the International Energy Agency (IEA).

However, fossil fuels continue to supply nearly 80% of world energy use through 2040. Natural gas is the fastest-growing fossil fuel, as global supplies of tight gas, shale gas, and coalbed methane increase. per year over the projection period, but remain a relatively minor share of total liquids supply through 2040.

The model has four sub-components: vehicle, fuel production, electricity grid; and energy supply. Among their findings were: RFS2 is satisfied at extreme oilprices (at least $215/barrel). This oilprice encourages biofuel use in the RFS2 timeframe, but not in the long run. —Westbrook et al. Barter, Dawn K.

Accenture has identified 12 technologies that it concludes have the potential to disrupt the current views of transport fuels supply, demand and GHG emissions over the next 10 years. by 2014) and also examines different global markets. Will be competitive at an oilprice of $45 to $90 at their commercial date.

On September 10 th , the EIA reported a production decline in the Lower 48—essentially shale production—of 208,000 BOPD (barrels of oil per day). That is a staggeringly enormous number, approximately 10 percent of the estimated global over-supply. And markets won’t wait to adjust pricing until we hit a balance.

No EDV deployment occurs with high battery costs, low oilprices, and no CO 2 policy. higher oilprices, a CO 2 policy, lower battery cost—the median market shares increase. higher oilprices, a CO 2 policy, lower battery cost—the median market shares increase. —Babaee et al.

FedEx joins Southwest Airlines, which signed a purchase agreement with RedRock in November 2014 for about 3 million gallons per year, in purchasing Red Rock’s total planned available volume of jet fuel. The agreement runs through 2024, with first delivery expected in 2017. Earlier post.).

In 5 of the 10 cities for which EIA collects weekly retail price data, gasoline prices exceeded $3.00/gal Rising crude oilprices and high levels of gasoline demand contributed to rising gasoline prices from January through May. gal at least once in 2018. per gallon between October and December.

With its headquarters in Vienna, Austria, one of the mandates of 12-member OPEC is to “ensure the stabilization of oil markets in order to secure an efficient, economic and regular supply of petroleum to consumers, a steady income to producers, and a fair return on capital for those investing in the petroleum industry.” Iraq’s Issues.

US regular gasoline retail prices averaged $2.78 In June, monthly retail gasoline prices averaged $3.06/gal, gal since October 2014 (in nominal terms). EIA forecasts regular-grade gasoline prices to average $2.92/gal per gallon (gal) in 1H21, compared with an average of $2.20/gal gal in 1H20. gal in 2H21 and $2.74/gal

A flood of bearish news has pushed down oilprices to their lowest levels in months, with WTI nearing $45 per barrel and Brent flirting with sub-$50 territory. With a bear market back, there is pessimism throughout the oil markets. However, the WTI/Brent spread has shrunk more dramatically since the collapse in oilprices.

The party is over for tight oil. Despite brash statements by US producers and misleading analysis by Raymond James, low oilprices are killing tight oil companies. Reports this week from IEA and EIA paint a bleak picture for oilprices as the world production surplus continues. Click to enlarge.

Saudi Arabia has increased production by 700,000 barrels per day since the fourth quarter of 2014 in an effort maintain market share. The resulting crash in oilprices is forcing some production out of the market, and Saudi Arabia intends for the brunt of that to be borne by others. There are several reasons for this.

In contrast to what some media sources are suggesting, oil and gas demand will not diminish, on the contrary, oil and gas prices will rise due to a lack of supply. The latter is partly caused by “global warming constraints” and lower oilprices in general. Link to article: [link].

Lower crude oilprices and strong demand for petroleum products, primarily gasoline, both in the United States and globally, have led to favorable margins that encourage refinery investment and high refinery runs. Total US motor gasoline product supplied is up 2.9% through the first five months of the year compared with 2014.

This sharp slowdown in activity in the conventional oil sector was the result of reduced investment spending driven by low oilprices. The slump in the conventional oil sector contrasts with the resilience of the US shale industry. With global demand expected to grow by 1.2

The main effect of this change on the forecasted STEO liquid fuels market balances is that the higher consumption in 2014 raises the baseline to which the STEO forecast benchmarks. Most of China’s methanol supply is from domestic production. MTG units involve high capital costs and are only cost-competitive when oilprices are high.

AEO2015 presents updated projections for US energy markets through 2040 based on six cases (Reference, Low and High Economic Growth, Low and High OilPrice, and High Oil and Gas Resource) that reflect updated scenarios for future crude oilprices. trillion cubic feet (Tcf) in the Low OilPrice case to 13.1

The United States was the largest source of LNG supply growth in 2021, adding 25 million metric tons (MMt) amid continued buildup of liquefaction capacity as well as the ramping up of output from plants turned down the previous year. MMt set in 2014. Total loaded LNG supply in 2021 reached 396.3 MMt, up 5.5% increase or 1.6

Oilprices have rebounded strongly since March. The benchmark WTI prices soared by more than 36 percent in two months, and Brent has jumped by more than 25 percent. In the Bakken, oil production actually increased by 1 percent in the month of March, a surprise development reported by the North Dakota Industrial Commission.

But while it produces at similar levels as Russia and the US, it is long been a vastly more influential player in the oil world. That is because of two reasons—the size of its reserves, and the ability to use latent spare capacity to quickly adjust supply, affording it an outsized influence on crude oilprices.

The report, “ Renewable Power Generation Costs in 2014 ”, concludes that biomass, hydropower, geothermal and onshore wind are all competitive with or cheaper than coal, oil and gas-fired power stations, even without financial support and despite falling oilprices. —“Renewable Power Generation Costs in 2014”.

United has also negotiated a long-term supply agreement with Fulcrum and, subject to availability, will have the opportunity to purchase at least 90 million gallons of sustainable aviation fuel a year for a minimum of 10 years at a cost that is competitive with conventional jet fuel.

Estimated US supply of PEVs from 2011-2015. and model 2011 2012 2013 2014 2015. The cumulative impacts of the various policy initiatives, the experience of the early purchasers of electric-drive vehicles and future oilprices will all play a role in determining future consumer demand. Fisker Karma EREV. Fisker Nina EREV.

It uses linear programming to estimate energy supply shifts over a multi-decadal timeframe, finding the least-cost means to supply specified demands for energy services subject to user-defined constraints, assuming a fully competitive market.

World petroleum and other liquid fuels consumption will increase 38% by 2040, spurred by increased demand in the developing Asia and Middle East, according to the Reference Case projections in International Energy Outlook 2014 ( IEO2014 ), released by the US Energy Information Administration (EIA). oil shale), and refinery gain.

This year, shale output forecasts combine with OPEC’s production cuts, geopolitical factors, and unexpected outages to further complicate supply/demand and oilprice forecasts by Wall Street’s major investment banks. shale production, new oil discoveries, and new project start-ups also differ a lot. shale output.

The first commercial-scale facilities with a potential production capacity of 1 million gallons will likely come online in the 2014 to 2016 window, Pike forecasts, although construction delays, a lack of capital, and lingering investment risk could potentially obstruct growth. Algae’s ultimate threat is over-hype.

Reflecting slow growth in travel and accelerated vehicle efficiency improvements, US light-duty vehicle (LDV, cars and light trucks) energy use will decline sharply between 2012 and 2040, according to the US Energy Information Administration’s (EIA’s) Annual Energy Outlook 2014 (AEO2014) Reference case released today. Tcf in 2012 to 2.1

The expanded upgrader capacity would be supplied by bitumen from the undeveloped Aurora South mine. Construction on a second mining train is planned to begin around 2014 with production commencing towards the end of the decade.

Critics cite the steep crude oilprice discounts for Canadian producers in the past year as further evidence that rail is not economic. On average in 2012, the price of heavy oils sands was $27 per barrel lower than a comparable barrel on the US Gulf Coast (USGC), and for short periods the difference was more than $40 per barrel.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content