This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The collapse in world oilprices in the second half of 2014 will have only a moderate impact on the fast-developing low-carbon transition in the world electricity system, according to research firm Bloomberg New Energy Finance. However, the slump in the Brent crude price per barrel from $112.36 on 30 June to $61.60

Oilprices fell back suddenly over the last few trading sessions, dragged down by some forces beyond the oil market. dollar has helped drive up crude prices for weeks , but that came to an abrupt halt last week. A rebound for the greenback led to a steep decline in oilprices on Friday.

The four-week rolling average of US crude oil export volumes has not fallen below 2.00 million b/d during the past three years, despite the COVID-19 pandemic, which caused significant crude oilprice drops, reduced demand, and reduced production in US and global oil markets. b lower than the Brent price.

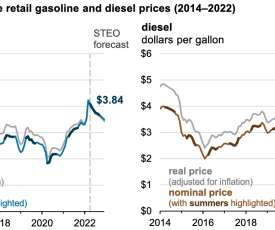

The US Energy Information Administration (EIA) forecasts that retail gasoline prices will average $3.84 per gallon this summer driving season—April through September—compared with last summer’s average price of $3.06/gal. EIA expects higher fuel prices this summer as a result of higher crude oilprices.

Two diametrically opposed views dominate the current debate about where the oilprice is heading. But, WoodMackenzie says, many of these still-to-be-launched projects are uneconomical at oilprices in the $50s per barrel, meaning that they should not be expected to get the all-clear anytime soon. Since (non-U.S.

Add to that a new report from the US government’s Energy Information Administration (EIA), which also cut its 2015 forecast for growth in global oil demand by 240,000 barrels per day, down to 880,000 barrels per day. For 2014, the EIA expects demand will be about 960,000 barrels per day. And yet on Nov.

It may be difficult to look beyond the current pricing environment for oil, but the depletion of low-cost reserves and the increasing inability to find major new discoveries ensures a future of expensive oil. The IEA predicts that the oil industry will need to spend $850 billion annually by the 2030s to increase production.

The impact of rising oilprices on North American light tight oil (LTO) production is said to be a “Catch 22”, the title of Joseph Heller’s popular 1961 novel set in WWII. Too many analysts continue to believe drilling and service has the same problem with rising oilprices. by David Yager for Oilprice.com.

Predicting and diagnosing the trajectory of oilprices has become something of a cottage industry in the past year. But along with all of the excess crude flowing from the oil patch, there is also an abundance of market indicators that while important, tend to produce a lot of noise that makes any accurate estimate nearly impossible.

Oilprices appear to be stuck in the $50s per barrel, but that doesn’t mean there aren’t serious supply risks to the market. An unexpected disruption could occur at any moment, as has happened in the past, leading to a sudden and sharp jump in prices. by Nick Cunningham for Oilprice.com.

The OPEC published its World Oil Outlook 2015 (WOO) in late December, which struck a much more pessimistic note on the state of oil markets than in the past. On the one hand, OPEC does not see oilprices returning to triple-digit territory within the next 25 years, a strikingly bearish conclusion.

Lest we be too quick to forget whence we came, America is now 9-months into lower gasoline prices, which started their swoon the week of June 30, 2015 from a lofty national average just under $3.70, tumbling almost every subsequent week before bottoming and bouncing from $2.02 the end of January, according to gasbuddy.com.

Those claiming that oil will continue to fall from here and remain low for evermore, however, are flying in the face of both history and common sense. The question we should be asking ourselves is not if oilprices will recover, but when they will.

million barrels daily, including from Russia, to reverse the free fall of oilprices. Now, many OPEC members are both desperate while not yet recovered from the 2014 blow. A recent report from Capital Economics said Saudi Arabia has its problems but it could withstand lower oilprices without feeling too much of a pinch.

Back when the onslaught began, which I mark as Thanksgiving Day 2014—when OPEC declined to cut—Wall Street began talking of shale as being a switch; as in you can turn it on and off. Back in the good old days—2012 or so—a single stage on a shale job was being priced at $125,000 or more. That’s underwater.

The average US household will spend about $550 less on gasoline in 2015 compared with 2014, as annual motor fuel expenditures are on track to fall to their lowest level in 11 years, according to projections by the US Energy Information Administration (EIA). The price for US regular gasoline has fallen 11 weeks in a row to an average $2.55

A continuing sharp decline in technology costs—particularly in solar but also in wind—meant that every dollar invested in renewable energy bought significantly more generating capacity in 2014. A key feature of the 2014 result was the rapid expansion of renewables into new markets in developing countries.

No EDV deployment occurs with high battery costs, low oilprices, and no CO 2 policy. higher oilprices, a CO 2 policy, lower battery cost—the median market shares increase. higher oilprices, a CO 2 policy, lower battery cost—the median market shares increase. —Babaee et al.

Calumet intends to provide the majority, if not all of the funding for this project, and to start production in the second half of 2014. Any remaining funding will be provided by Calumet’s other project partners.

Among their findings were: RFS2 is satisfied at extreme oilprices (at least $215/barrel). This oilprice encourages biofuel use in the RFS2 timeframe, but not in the long run. The simulation evolves the LDV parc, stepping through 2050, although most of the analysis in the paper focuses on simulations through 2022.

Today’s weak economic environment has reduced expectations of oil demand growth for the medium term, yet the reallocation of demand by region and key product, which has been underway for the last 15 to 20 years, is expected to continue. Demand from non-OECD economies is forecast to overtake that in the OECD as early as 2014.

The current plunge in oilprices will likely negatively affect plug-in and hybrid vehicle sales in the short term; automakers such as BMW are already warning of lower sales of plug-in vehicles given the market context. Anticipated price of oil and forecast plug-in sales. Lux on the price of oil.

The low levels in discoveries come as a result of a pullback during the past 10 years in the wildcat drilling that targets conventional oil and gas plays—most drastically after oilprices collapsed in 2014. —Keith King, senior advisor at IHS Markit and a lead author of the IHS Markit E&P trends analysis.

Despite what appears to be a saturated oil market in 2014, oil producers around the world will struggle to meet rising demand over the next few decades. Under that assumption, oilprices would rise only a modest amount over that timeframe. by Nick Cunningham of Oilprice.com. million bpd by 2035.

Simply put, the world has too much oil at the moment which has resulted in the reduction of price levels from approximately $100 to $50 a barrel, and OPEC (as well as US shale producers) has a major role to play in this supply glut. It also has the fifth largest proven crude oil reserves in the world.

The Brent crude oil spot price averaged $112 per barrel in 2012, and EIA’s July 2013 Short-Term Energy Outlook projects averages of $105 per barrel in 2013 and $100 per barrel in 2014.

In 5 of the 10 cities for which EIA collects weekly retail price data, gasoline prices exceeded $3.00/gal Rising crude oilprices and high levels of gasoline demand contributed to rising gasoline prices from January through May. gal at least once in 2018. per gallon between October and December.

Since late 2014, the production of crude oil has outpaced demand, triggering a sustained collapse in world oilprices, which have remained mostly below $50 per barrel. As a result, these low prices have put pressure on the market for natural gas vehicles (NGVs) and the corresponding refueling infrastructure.

Between January 2016 and March 2017, oil production in the Permian Basin increased in all but three months, even as domestic crude oilprices fell. As production in other regions fell throughout most of 2015 and 2016, the Permian provided a growing share of US crude oil production.

Saudi Arabia has increased production by 700,000 barrels per day since the fourth quarter of 2014 in an effort maintain market share. The resulting crash in oilprices is forcing some production out of the market, and Saudi Arabia intends for the brunt of that to be borne by others. There are several reasons for this.

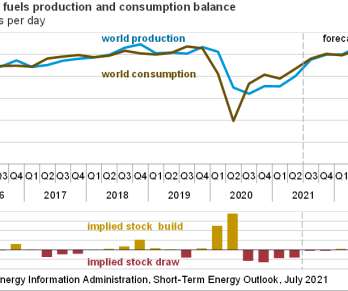

US regular gasoline retail prices averaged $2.78 In June, monthly retail gasoline prices averaged $3.06/gal, gal since October 2014 (in nominal terms). EIA forecasts regular-grade gasoline prices to average $2.92/gal per gallon (gal) in 1H21, compared with an average of $2.20/gal gal in 1H20. gal in 2H21 and $2.74/gal

Many oil companies had trimmed their budgets heading into 2015 to deal with lower oilprices. But the collapse of prices in July—owing to the Iran nuclear deal, an ongoing production surplus, and economic and financial concerns in Greece and China—have darkened the mood. That could cause oilprices to spike.

The party is over for tight oil. Despite brash statements by US producers and misleading analysis by Raymond James, low oilprices are killing tight oil companies. Reports this week from IEA and EIA paint a bleak picture for oilprices as the world production surplus continues. percent in August 2015.

A flood of bearish news has pushed down oilprices to their lowest levels in months, with WTI nearing $45 per barrel and Brent flirting with sub-$50 territory. With a bear market back, there is pessimism throughout the oil markets. However, the WTI/Brent spread has shrunk more dramatically since the collapse in oilprices.

The oil majors reported poor earnings for the fourth quarter of last year, but many oil executives struck an optimistic tone about the road ahead. The collapse of oilprices forced the majors to slash spending on exploration, cut employees, defer projects, and look for efficiencies. per barrel, rising to $36.50.

Oil companies continue to get burned by low oilprices, but the pain is bleeding over into the financial industry. Major banks are suffering huge losses from both directly backing some struggling oil companies, but also from buying high-yield debt that is now going sour. by Nick Cunningham of Oilprice.com.

The official chatter is that the OPEC meeting in Algeria from September 26 to 28 could conclude with an agreement to freeze production by the member nations, with even Russia joining forces in a freeze that may prevent further oilprice erosion. The oil-rich nation underestimated the resilience of the U.S.

According to a separate report from SAFE, a Washington-based think tank, the oil industry has cut somewhere around $225 billion in capex in 2015 and 2016, which will lead to global supplies 4 million barrels per day lower in 2018-2020, compared to what market analysts expected as of 2014. The price acts as a self-correcting mechanism.

The report, which covers US airlines in domestic operations in 2014, highlights a continuing gap in the carbon intensity of US carriers, and comes as the International Civil Aviation Organization (ICAO) meets in Montreal to debate proposals that will serve as the basis for future US regulation. from 2013 to 2014. Earlier post.)

In the last quarter of 2014, in the face of possible oversupply, Saudi Arabia abandoned its traditional role as the global oil market’s swing producer and therefore it role as unofficial guarantor of existing ($100+ per barrel) prices. Prices rebounded to $60 for a few months, before falling once again below $50.

Argentina offers one of the few places on earth where oil companies are not suffering from the full force of the collapse in prices. Argentina regulates oilprices, a policy originally intended to insulate the public from the whims of the market, protecting people from triple-digit crude prices.

Subsequently, the company used data on electricity and oilprices; government incentives; charging infrastructure; vehicle costs; and other factors to determine the business case of an electrified vehicle (HEV, PHEV, or BEV) purchase against its conventional competitor in each forecast year.

If You’re a Free Range Oil Producer. Despite low oilprices, Saudi Arabia is maintaining its investment in its oil industry. as the drop in oilprices over the last year has put a strain on the nation’s finances.". In a CNN article quoting SIPRI for 2014, the author's guesses for 2015 (6.25

Instead it pursued a strategy of fighting for market share, contributing to an immediate rout in oilprices. OPEC is widely expected to continue its current strategy at its next meeting, and as such, no rebound in oilprices is expected, at least not because of the results of the group’s meeting in Vienna.

We organize all of the trending information in your field so you don't have to. Join 5,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content